Back when factor research meant tenure, it was commonplace to use a monthly rebalancing schedule. Higher frequency data was hard to come by and even harder to clean. Compute was expensive and it was something to be conserved. Transaction costs were prohibitive. So, it made sense. However, things have changed a lot since the 90’s. In addition to asking how many months should go between rebalancing, we can now ask how many weeks?

While data and compute are plentiful, trading costs haven’t really gone away. We have an STT of 0.1%, exchange fees and taxes that all add up to a significant drag on net returns. So, once we layer-in costs, higher frequency strategies require a process that generate highly overlapped portfolios.

Contrast the simple momentum version (Momentum Rebalance Frequency, Part II) to the Prophet version (Prophet for Momentum, Part II). Even if you were to tune Prophet on the prediction side of things, unless you incorporate a transaction cost penalty, it is likely that most of the excess returns leaks away as costs.

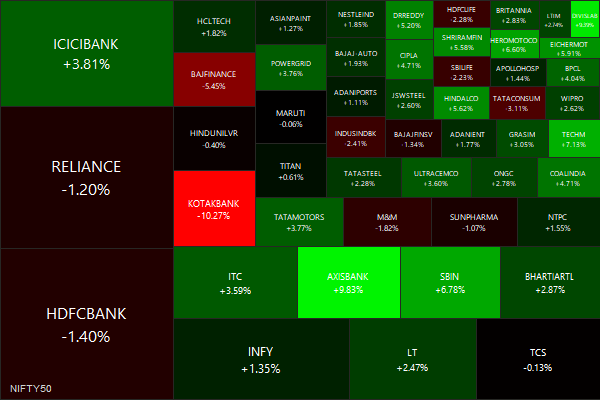

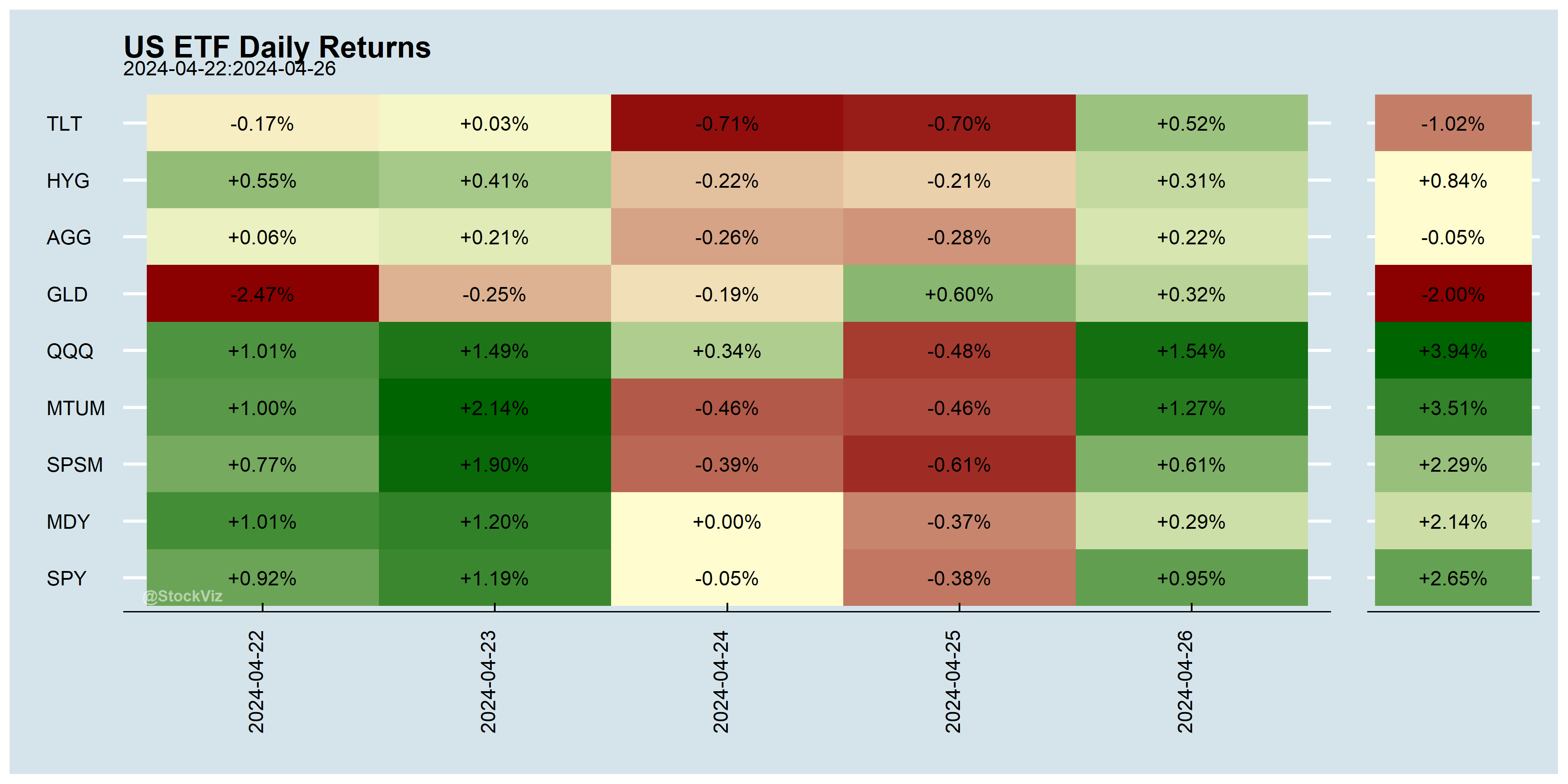

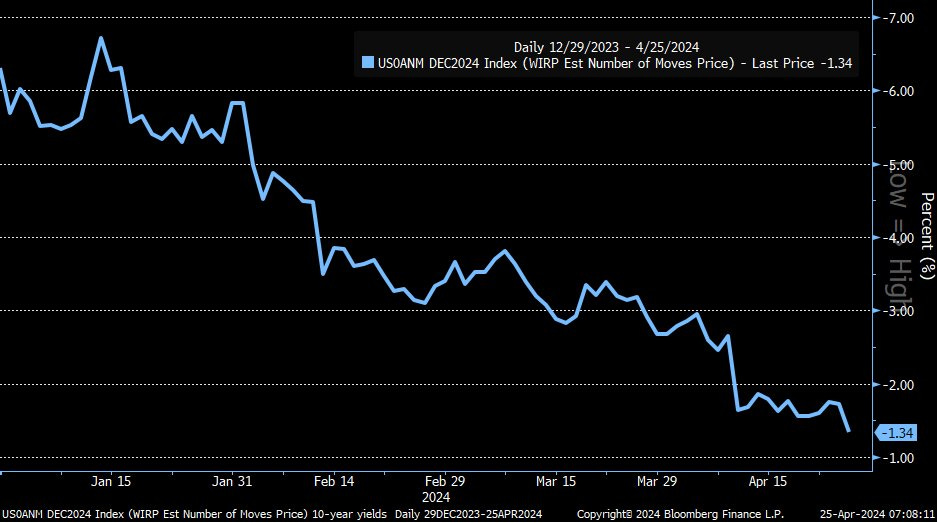

Markets this Week

More here: country ETFs, fixed income, currencies and commodities.

Links

Research

Same-Weekday Momentum (SSRN)

A disproportionately large fraction (70%) of stock momentum reflects return continuation on the same weekday (e.g., Mondays to Mondays), or the same-weekday momentum. We provide direct and novel evidence that links it to within-week seasonality and persistence in institutional trading. Overall, our findings highlight institutional trading as an important driver of the stock momentum.

Trading Volume Alpha (SSRN)

Portfolio optimization chiefly focuses on risk and return prediction, yet implementation costs also play a critical role. We focus on a key, yet general, component of trading costs that abstracts from these challenges---trading volume. Trading volume is highly predictable, especially with machine learning. We model the economic benefits of predicting volume through a portfolio framework that trades off portfolio tracking error versus net-of-cost performance---in essence translating volume prediction into net-of-cost portfolio alpha. We find the benefits of predicting volume to be substantial, and potentially as large as those from return prediction.

Overnight PEAD and SEC Form 8-K Disclosures (SSRN)

Companies reporting extreme quarterly earnings misses exhibit pronounced significant overnight drift post-announcement. We hypothesize that extreme earnings misses stimulate more intensive information acquisition throughout the reporting quarter, as those earnings announcements resolve a smaller fraction of information uncertainty. Using post-announcement SEC Form 8-K disclosures to proxy for additional material information, we show that information acquisition activities become more prevalent and substantial following extreme earnings misses. Concomitantly, the implied volatilities of these stocks remain elevated for much of the earnings quarter. Moreover, the incremental post-announcement Form 8-K information is unscheduled, mostly arriving overnight when market liquidity is low. These factors contribute to a higher overnight risk premium, and thus a pronounced average overnight drift post-earnings announcement.

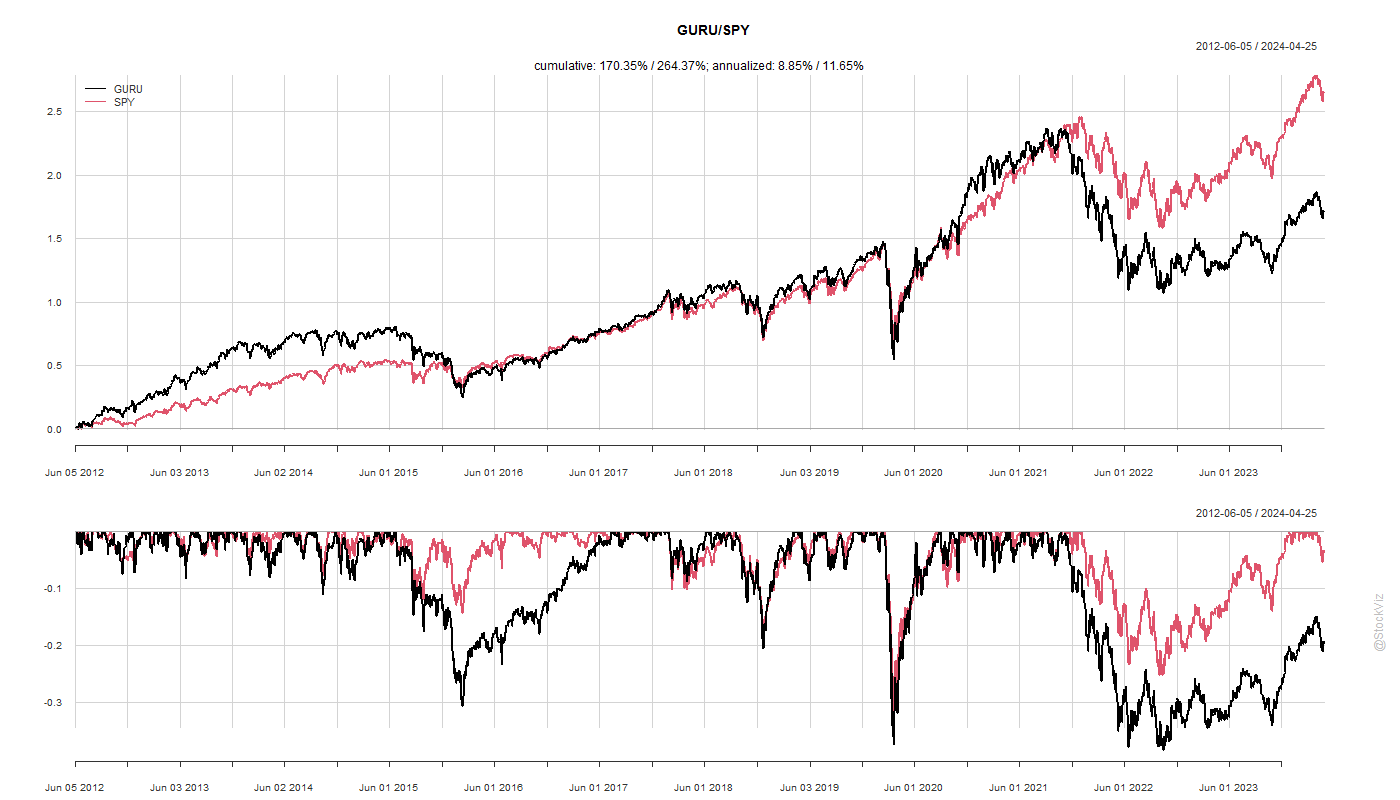

Outperforming the Market: Cloning from SEC 13F Filings (SSRN)

Our findings demonstrate that cloned portfolios in the top quartile, derived from SEC EDGAR Form 13F filings, replicate the funds' performances and exceed the SP500 index by 24.25% on an annualized risk-adjusted basis.

Hope triumphs over experience:

Do Political Connections Pay for Pledging of Shares: Evidence from India (SSRN)

This study explores the stock-pledging conduct of promoters or controlling shareholders in Indian companies with political affiliations. Using a sample of publicly listed companies on the National Stock Exchange (NSE) in India, covering the period from 2009 to 2019, we investigate how the capital generated from promoters' stock pledging influences their investment decisions in higher-risk projects. The results reveal a significant reduction in corporate investments among firms involved in stock-pledging activities. However, promotors of politically connected firms actively engaging in stock-pledging tend to invest in projects with elevated risk. Furthermore, politically affiliated firms demonstrate lower volatility in stock returns than their non-connected counterparts. These findings suggest that firms' political connections serve as a protective factor, mitigating both investment risk and the volatility of returns.

Investing & Economy

India

The India express - The Economist Special Report (economist)

Indian companies directly or indirectly in business with European firms face a twin hurdle as Germany tightens its screws on a new law aimed at ensuring fair labour standards and environmental requirements. (livemint)

The RBI has been on a streak lately - the body count so far: reuters.

RoW

Water is more valuable than oil. In an unprecedented deal, a private company purchased land in a tiny Arizona town – and sold its water rights to a suburb 200 miles away. Local residents fear the agreement has ‘opened Pandora’s box’ (theguardian).

Boeing’s problems were as bad as you thought (vox)

As a concrete reflection of Boeing’s importance to the broader economy, the U.S. government should be prepared to co-finance a new Boeing model, with risk-sharing in which the U.S. government gets a stake in the success of the new design in return for its financial support. And Boeing needs to swallow its pride and accept that it now needs what aviation insiders will recognize as “launch aid,” or—in dry European bureaucratic jargon, repayable launch investment.

Boeing and the Dark Age of American Manufacturing (theatlantic)

Meta’s battle with ChatGPT begins now (theverge)

Apple's smartphone shipments in China tumbled 19% in the first quarter of the year, the worst performance since 2020, as the iPhone maker took a hit from Huawei's new product launches in the premium segment. Apple's share in the world's biggest smartphone market fell to 15.7% in the first quarter from 19.7% a year earlier. (reuters)

Risk parity funds have lagged global 60/40 funds every year since 2019. That’s driven investors to pull out cash, cutting the amount in such funds to about $90 billion by the end of 2023 from a peak of about $160 billion in 2021 (yahoo).

Tesla’s Autopilot and Full Self-Driving linked to hundreds of crashes, dozens of deaths (theverge).

Faced with global competition from countries with cheap renewable energy, the EU should embrace a partial deindustrialisation rather than subsidise uncompetitive industries (euractiv)

China has more than 100 factories with the capacity to build close to 40 million internal combustion engine cars a year. That is roughly twice as many as people in China want to buy, and sales of these cars are dropping fast as electric vehicles become more popular. Dozens of gasoline-powered vehicle factories are barely running or have already been mothballed. (nytimes)

Odds & Ends

New research has uncovered a social world of viruses full of cheating, cooperation and other intrigues, suggesting that viruses make sense only as members of a community. (quantamagazine)

Meme of the Week