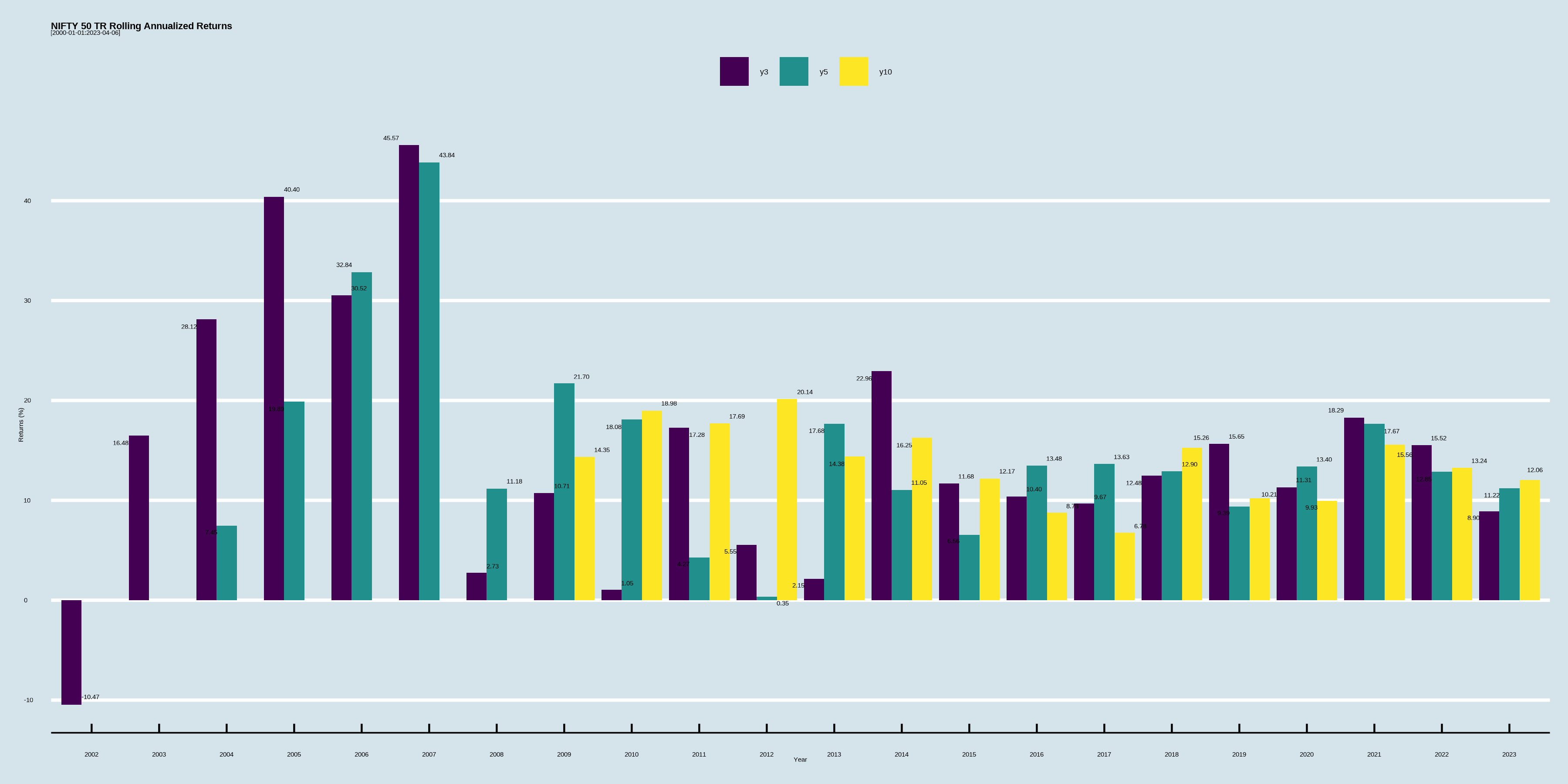

Remember the first baby steps you took in the market? Chances are that experience ends up shaping your expectations from the market for the rest of your life.

Ask anyone who was active in the markets in the 2000s as to what kind of returns you should expect. Their answer will be completely different from someone who entered the market a decade later.

NIFTY’s 10-year return in 2010 was 19%. 2005-2007 was completely nuts. Pan to 2020 and you end up with a 10% 10-year return — downright depressing.

This is the dilemma that every investor faces while trying to come up with a reasonable estimate of future returns - do you extrapolate the long-term average or do you pick only the last few years and smooth them out? After all, we are probably never going to see the “India Shining” era ever again, right?

Things get tricker when a benchmark index has never had a 10-year period without double-digit returns. What should an Indian MIDCAP investor expect?

Ideally, you should model a reasonably wide range of outcomes and be happy with whatever you get. If you are looking for certainty, the market is the wrong place to go looking for it.

Markets this Week

A holiday shortened week ended mostly green with the RBI going on a surprise pause.

More here: country ETFs, fixed income, currencies and commodities.

Links

Research

The significance of each factor changes drastically over time and only 3 clusters of factors that have incremental information.

Useful Factors Are Fewer Than You Think (ssrn)

The performance of almost all groups of factors can be improved through timing, with improvements being highest for profitability and value factors. Past factor returns and volatility stand out as the most successful individual predictors of factor returns.

Timing the Factor Zoo (ssrn)

~

US Macro

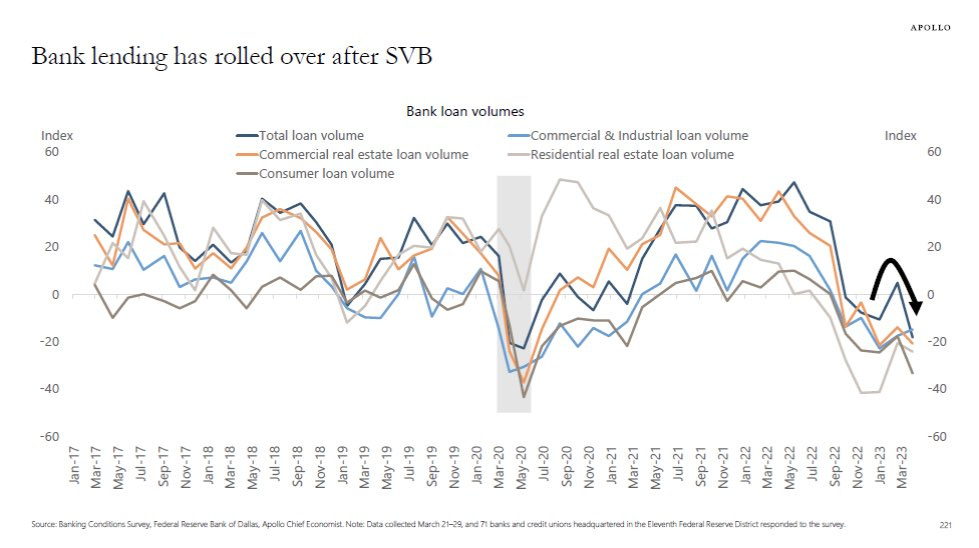

The credit crunch has started. .. A survey of 71 banks in the Dallas Fed district done after SVB went under shows a dramatic reversal in loan volumes, .. from March 21 to 29.

~

Indian Macro

India's services exports rose 24.5% on year in October-December 2022, hitting a record $83.4 billion during the quarter… largely powered by global capability centres, which have started to offer global clients a range of high-end and critical solutions such as accounting and legal support. (reuters)

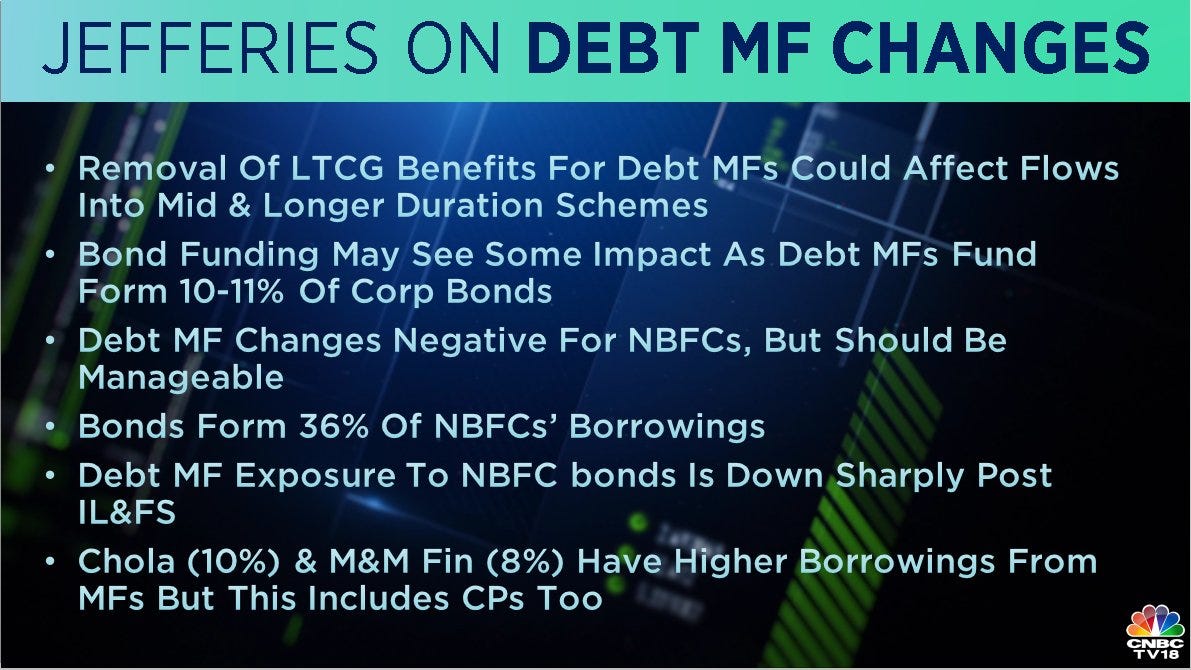

India's decision to take away long term tax benefits for debt mutual funds is likely to weaken demand for longer duration corporate bonds. (reuters)

~

A guaranteed pension to all government employees is an insult on top of injury.

While more than 80 per cent of the labour force works in the informal sector with practically no job security and old-age financial support, the 5-6 per cent of the workforce that worked for the government enjoyed job security and very generous post-retirement benefits.

~

No. You did not find the next Amazon.

The 21st Century Amazon investing experience has led to a generation of investors being way too patient in my opinion with profitless prosperity, granting way too many mulligans to companies that have flawed business models. Sure, it’s easy to grow revenues when you sell a product or service for less than it costs to produce it. But when you try to raise the price to cost plus a profit, often consumers won’t see the price-value relationship anymore.

The thing that is so funny to me about everyone chasing the repeat Amazon dream, hoping that profitless prosperity will transform into a trillion-dollar market cap yet again, is that the success of the AMZN stock price has very little to do, in my opinion, with the once loss-making e-commerce business turning wildly profitable. It has everything to do with Amazon starting a new business that turned out to be wildly profitable: AWS (Amazon Web Services).

~

AI will generate consumer surplus. But don’t expect it to boost corporate profits.

~

The interiors of our homes, coffee shops and restaurants all look the same. The buildings where we live and work all look the same. The cars we drive, their colours and their logos all look the same. The way we look and the way we dress all looks the same. Our movies, books and video games all look the same. And the brands we buy, their adverts, identities and taglines all look the same.

But it doesn’t end there. In the age of average, homogeneity can be found in an almost indefinite number of domains.

The Instagram pictures we post, the tweets we read, the TV we watch, the app icons we click, the skylines we see, the websites we visit and the illustrations which adorn them all look the same. The list goes on, and on, and on.

Meme of the Week