Limits of Arbitrage

perfection is theoretical

Just because something shouldn’t exist because of an arbitrage mechanism doesn’t mean that it doesn’t exist. For example, Authorized Participants are supposed to continuously close the gap between an ETF’s price and NAV through the Creation and Redemption process (nseindia, ssga). Theoretically, the closing price of an ETF should be equal to the NAV of the corresponding fund. However, reality is something quite different (ETF Premium/Discount to NAV [2018])

Another example is the bid/offer spread. Theoretically, wide spreads on index futures should get arbed away. However, even fairly liquid contracts have varying spreads across expiries and time-of-day. We wrote about such an instance this week: Midcap Select Index Futures, Part II

Before you start trading an instrument, you should absolutely spend some time exploring the limits of arbitrage that theoretically applies to it. Here, there be monsters.

Markets this Week

Markets got whipped…

More here: country ETFs, fixed income, currencies and commodities.

Crypto mooned on ETF hopes…

Remember ARKK? Now at an 82% drawdown.

On 12/20/21 Cathie Wood announced to retail investors that $ARKK could return 40% / year for the next 5 years. Given its since down another 60%+ and almost 2 years have passed, it will need to return 160% / year for the next ~3 years to get there. @EconomPic

Links

Research

Factor Zoo (.zip)

The number of factors allegedly driving the cross-section of stock returns has grown steadily over time. We explore how much this ‘factor zoo’ can be compressed, focusing on explaining the available alpha rather than the covariance matrix of factor returns. Our findings indicate that about 15 factors are enough to span the entire factor zoo. This evidence suggests that many factors are redundant.

Venture Predation

A venture predator is a startup that uses venture finance to price below its costs, chase its rivals out of the market, and grab market share. Venture capitalists (VCs) are motivated to fund predation—and startup founders are motivated to execute it—because it can fuel rapid, exponential growth. Critically, for VCs and founders, a predator does not need to recoup its losses for the strategy to succeed. The VCs and founders just need to create the impression that recoupment is possible, so they can sell their shares at an attractive price to later investors who anticipate years of monopoly pricing. In this Article, we argue that venture predation can harm consumers, distort market incentives, and misallocate capital away from genuine innovations.

No Revenge for Nerds?

This paper compares the careers of Ivy League athletes to those of their non-athlete classmates. We find that Ivy League athletes outperform their non-athlete counterparts in the labor market. Athletes attain higher terminal wages and earn cumulatively more than non-athletes over the course of their careers controlling for school, graduation year, major, and first job. In addition, they attain more senior positions in the organizations they join. Collectively, our results suggest that non-academic human capital developed through athletic participation is valued in the labor market and may support the role that prior athletic achievement plays in admissions at elite colleges.

Economy & Investing

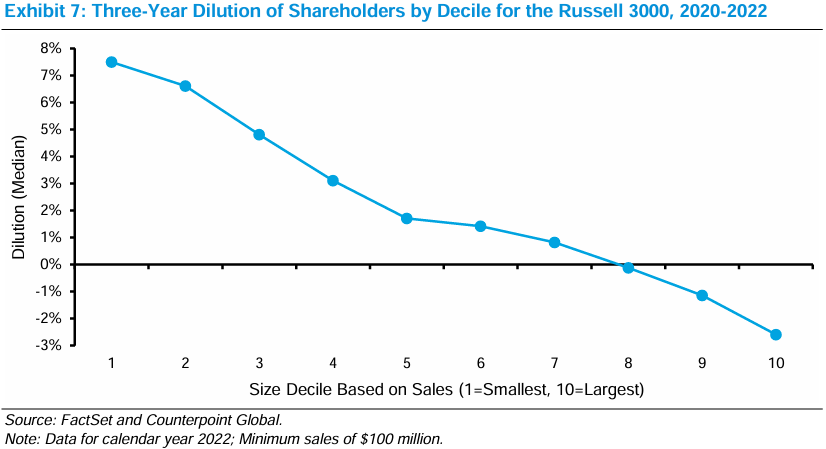

From Michael Mauboussin’s latest:

Shareholder dilution for companies in the Russell 3000, ranked in size by decile from 2020 to 2022. The Russell 3000 tracks the performance of the largest 3,000 U.S. public companies. The companies in the smallest three deciles realized average dilution of six percent, while the largest three deciles collectively retired equity.

~

India transitioned to T+1 settlement, where trades are settled within a day, in January. The Securities and Exchange Board of India (SEBI) now plans to allow instant settlement by October next year as an option running alongside T+1 settlement. (reuters)

Financial liabilities of households have risen faster than their assets, an indication of rising indebtedness. (thehindu)

India's central bank has urged lenders to tighten controls on tiny personal loans, particularly loans of up to 10,000 rupees ($120) taken for three to four months, often for "lifestyle" spending, following a surge in borrowing by low-income consumers. (reuters)

India's markets regulator and its central bank are investigating about a dozen cases of alternate investment funds (AIFs) allegedly being used to circumvent regulations, including "evergreening" of stressed loans. (reuters)

~

A law that allows low-price packages (under $800) to enter the U.S. duty-free and with little customs scrutiny has enabled the breakneck growth of two e-commerce companies with roots in China, Shein and Temu. (livemint)

~

Death from overfunding: An obituary for Convoy (freightwaves)

SmileDirectClub's journey over the years presents a case study in the volatility and challenges of startup scaling and market competition. After going public in 2019 with an initial valuation of $8.9 billion, the company recently filed for Chapter 11 bankruptcy. Despite raising $1.35 billion in its IPO, it listed $499 million in assets against more than $1 billion in liabilities at the time of the bankruptcy filing. (valuethemarkets)

Meme of the Week