The market is a complex dynamic adaptive system. The weather, for example, is a complex dynamic system. What makes the market tricky is the “adaptive” part. The collective actions of market participants changes the nature of the market over time.

Complex-dynamic systems can be modeled in super-computers. But, in spite of billions spent on weather stations, satellites, and hardware, forecasters max out at predicting the weather 5 days out and still struggle with micro-climates (i.e., is it going to rain on you today?)

If you try to model the market like the weather, the minute a forecast is made, the market will change. This adaptive nature of the market has confused and confounded the best minds for centuries. The minute you think you’ve figured something out, along comes a googly.

However, on a grand scale, there are only two things at work in the market: momentum and mean-reversion. Doesn’t matter if you are a fundamental investor or an options volatility arb, your positive expected value (+EV) comes from one of these two processes.

The market doesn’t care if you are a PhD in quantum physics or if you are a Noob drawing lines on a price chart. As long as you are harvesting one of the two effects, you’ll end up making money. This can get super frustrating to the Pros when the Noobs capture a large part of the +EV of a certain effect with sticks-and-stones while they are busy crunching PDEs on their supercomputers.

Welcome to the land of proxies.

Let’s say the Pros use an effect/event to run their strategy. Along comes a Noob who enters on a “pennant formation” and exits on a “reverse-flag formation” (yes, I’m making this up.) The problem is, given the nature of the markets, there is a good chance that the Noob might actually be harvesting the same underlying effect as the Pros. Maybe not all of it, but close enough to pocket some real cash. The Noob’s “pattern” is a proxy for the same underlying premia/arb that the Pros are looking at.

The drama starts when the two meet and exchange notes.

One such drama happened last week on the issue of stop-losses. The twitter exchange below tells you more about how people approach trading than it does about stop losses. Do give it a read.

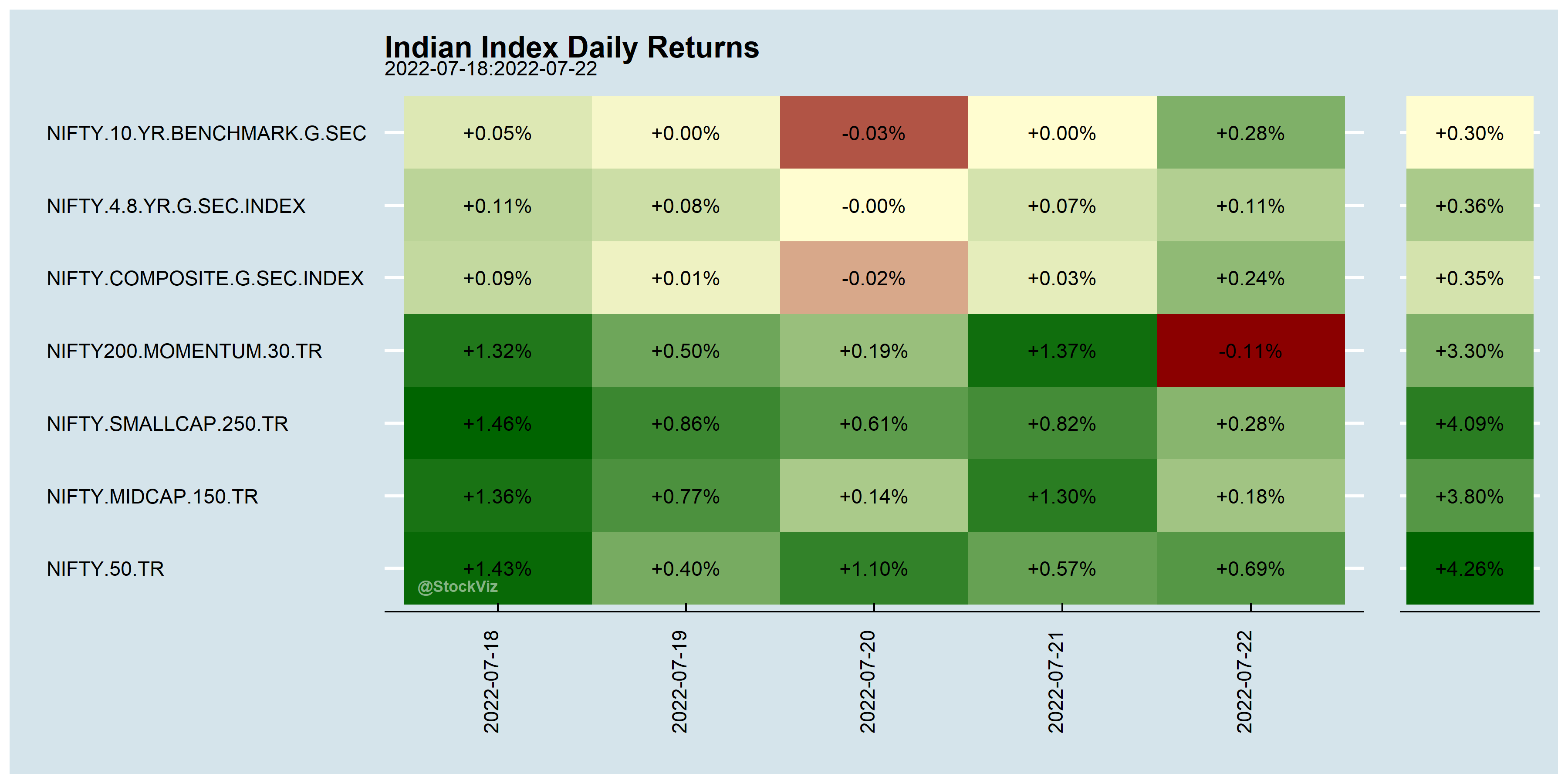

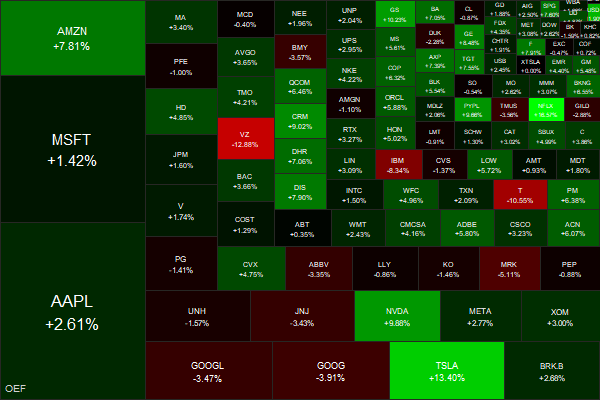

Markets this Week

This week reinforced my belief that the average retail investor should only look at their portfolio once a year, at tax time.

Links

Used solar panels and wind turbine blades are going straight into landfill. (hbr, bloomberg, abc)

~

Only fight wars that you can win.

~

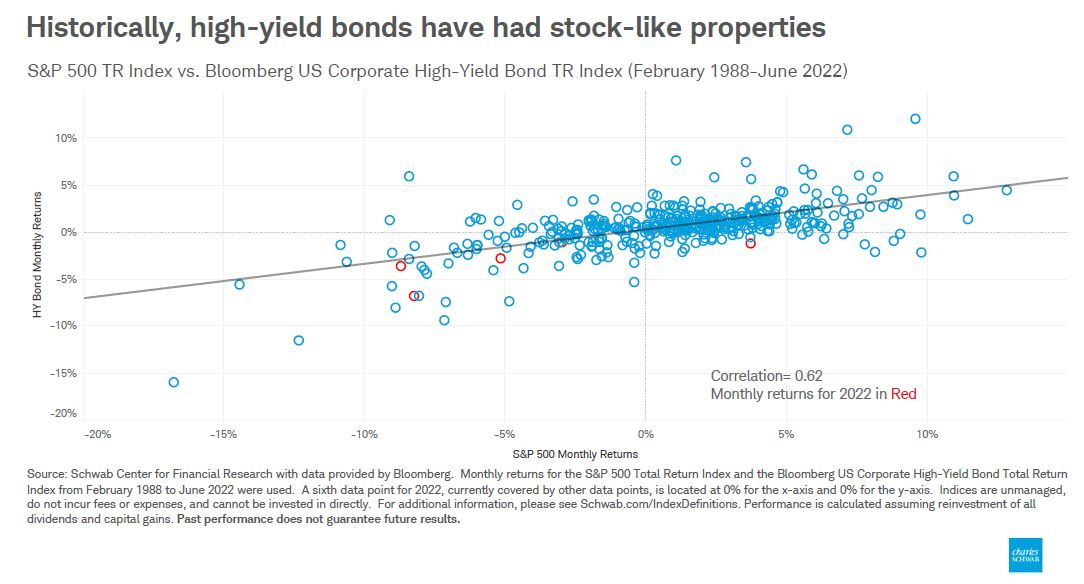

Bond-like returns with equity-like volatility.

~

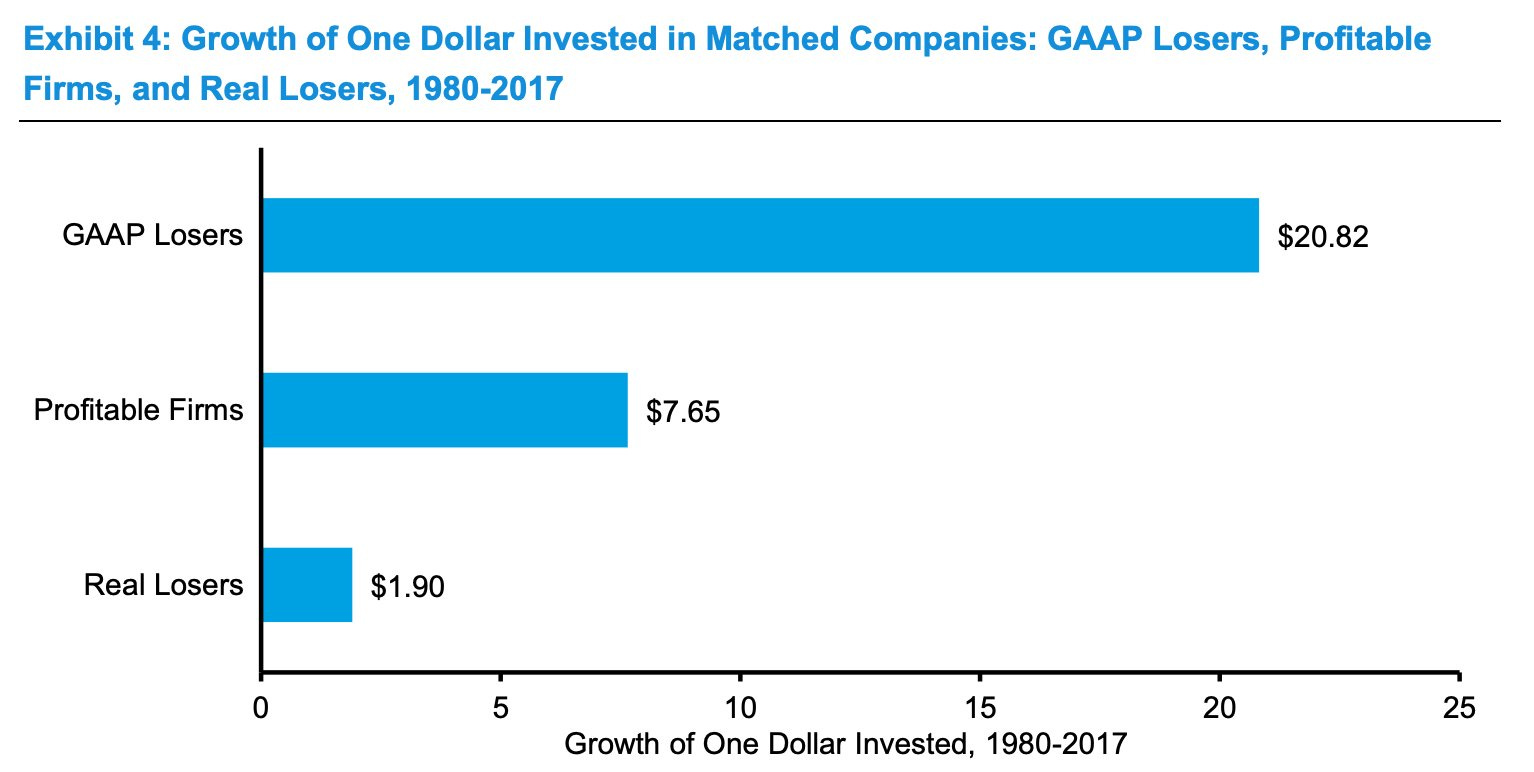

Accounting rules shape investor behavior. Exhibit ∞

~

~

What makes a DM a “D”M are institutions.

Latest data placed by the government in Parliament this week shows a rising number of people giving up Indian citizenship. In 2021, over 163,000 Indians chose to become citizens of other countries. This is the highest in seven years. (livemint)

~

Yes, there is such a thing as too much infrastructure.

~

Publish or Perish, they said.

“Nudge” became a multi-billion dollar business in its own right.

~

Looks like in the Angel investing/Venture Capital world, the real winners are the GPs.

~

Speaking of Ponzi schemes…

~