Skepticism vs. Cynicism

A skeptic tests while a cynic rests.

Investing requires a healthy dose of skepticism. There is usually nothing “new” to be said. Things that your granddad knew to work still works.

Buy things cheap (value),

buy things that are growing (GARP),

buy whatever most people are buying (momentum),

buy whatever is going up (trend following),

buy everything (index).

However, skepticism requires you to continuously test things out. It is the ultimate truth-finding mission.

For example, back in 2019, AQR published a paper showing that factors themselves exhibit momentum (Factor Momentum Everywhere). There were a lot of cynical takes on this at that time, broadly painting it as a noisy derivative of a derivative. While crowding is a thing, we were skeptical about its viability after transaction costs. So, we decided to test it out and setup up model portfolios. Turns out, given the constraints in specification at that time, our skepticism was warranted.

However, is three years enough to dismiss it? Probably not. Moreover, the US version of it (Factor Momentum III) is doing reasonably well.

Similarly, a lot of “value” investors are dismissive of trend-following. Will they change their mind when they realize that a trend overlay on a simple value strategy works well (e.g.: NIFTY500 VALUE 50)?

While there is indeed nothing “new” in investing, it shouldn’t stop you from trying to remix old tunes into something new. Serious investors are constantly probing, poking, testing and validating different strategies. Cynics take the easy way out.

Markets this Week

More here: country ETFs, fixed income, currencies and commodities.

Links

It’s all reflexive.

The stock market is seen as a reflection of what happens in the real world: A company releases poor earnings results and its stock price tanks, or shares rise if the firm becomes an acquisition target. But Wharton research shows that this is not the end of the road for the stock market’s impact; how the stock reacts in turn affects a company’s decision-making in a sort of feedback loop. And when corporate decisions are informed by the market, it leads to a higher market value for the firm. (wharton)

~

Google is feeling a bit of pressure from Microsoft’s AI chatbot pump. The pile-on begins.

How Google Ran Out of Ideas (theatlantic)

The maze is in the mouse (@pravse)

~

Macro takes:

USA

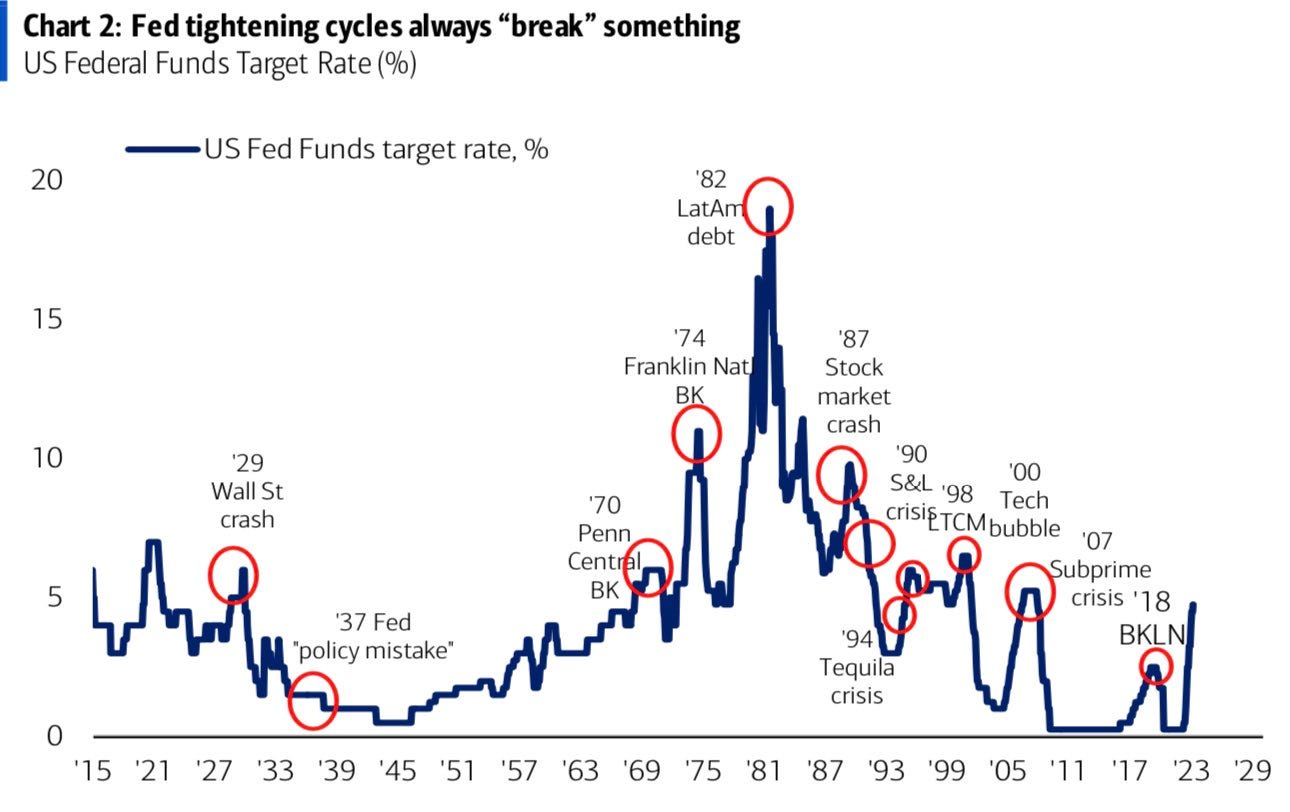

Volcker is remembered today as having the courage to run tight enough policy to break the back of inflation. That is a far too simple view. It took 3 years. Multiple times he thought he had succeeded and eased policy only to reignite inflationary pressures. He was criticized for being both too tight and too easy. It was never really clear what drove inflation, and only tighter money seemed to contain it. While in the end he was successful, it was an extremely difficult and volatile path. (unlimitedfunds)

Central bankers are worried that their economies—and especially their labour markets—are overheating. Though they are slowing the pace at which they raise interest rates, they are wary of repeating the mistakes of the 1970s, during which monetary policy was loosened in response to falling inflation only for prices to surge once more. (economist)

China

Pakistan

Japan

~

Good advice!